News

Simply Rescheduling Might Not Improve the Cannabis Banking Issues

When the news hit that cannabis might be rescheduled from Schedule I to Schedule III under the Controlled Substances Act, the industry (especially cannabis banking) was all over the place.

I mean, this would be huge for cannabis. Moving to Schedule III would mean cannabis has an accepted medical use, which would be a total 180. But despite the headlines, there’s one big problem the cannabis industry can’t ignore: banking.

Cannabis businesses have been trying to get and keep banking for years, and federal regulations make banks wary of working with them. Even with rescheduling, it’s not clear whether financial institutions will open their doors wide to the industry. In fact, rescheduling might not do much to solve the biggest problems in cannabis banking.

Here at 3CHI, we’re keeping our finger on the pulse of the biggest industry trends and news so our readers know about product education but also how big changes may (or may not) change the entire cannabis landscape.

Okay, let’s get started.

A Legislative Journey: From the SAFE Banking Act to the SAFER Banking Act

Efforts to address cannabis banking challenges have been ongoing for years, starting with the introduction of the Secure and Fair Enforcement (SAFE) Banking Act in 2019. The SAFE Banking Act aimed to provide legal protections for financial institutions working with state-legal cannabis businesses. Despite bipartisan support and multiple passes in the U.S. House of Representatives, the bill stalled in the Senate several times, largely due to political disagreements and its attachment to broader legislative packages.

Fast forward to 2023, when the cannabis industry saw renewed hope with the introduction of the Secure and Fair Enforcement Regulation (SAFER) Banking Act. S.2860, building on the framework of the SAFE Banking Act but further addresses key regulatory issues. The act clarifies that proceeds from legitimate state-licensed cannabis businesses are not to be considered proceeds of illegal activity, reducing the legal risks for financial institutions.

The SAFER Banking Act also includes provisions aimed at improving access to banking for smaller and minority-owned cannabis businesses, a response to criticism that earlier versions of the bill didn’t do enough to address equity in the industry.

In September 2023, the SAFER Banking Act passed the Senate Banking Committee, marking a significant milestone and demonstrating greater bipartisan support than in previous years. While the act still faces hurdles, its progress reflects a growing recognition in Congress of the need to provide the cannabis industry with access to basic financial services.

A Legal Gray Area: Rescheduling Doesn’t Fully Solve Cannabis Banking Problems

For banks and other financial institutions, working with cannabis businesses isn’t just risky; it’s legally complicated. Right now, under federal law, cannabis is a Schedule I substance (along with heroin), which means it has no accepted medical use and a high potential for abuse. Moving to Schedule III means it has medical benefits and lower abuse potential, but it’s still under the Controlled Substances Act.

As long as cannabis is under the Controlled Substances Act (even at Schedule III), financial institutions have to be careful. Federal regulators are still imposing strict oversight on banks working with cannabis businesses to ensure Bank Secrecy Act (BSA) compliance and other regulations. The BSA requires banks to file suspicious activity reports if money laundering is suspected.

To a bank, the risk of running afoul of these regulations—and facing fines, penalties, or even closure—is a big deterrent. So just because cannabis is rescheduled doesn’t mean the banking floodgates will open.

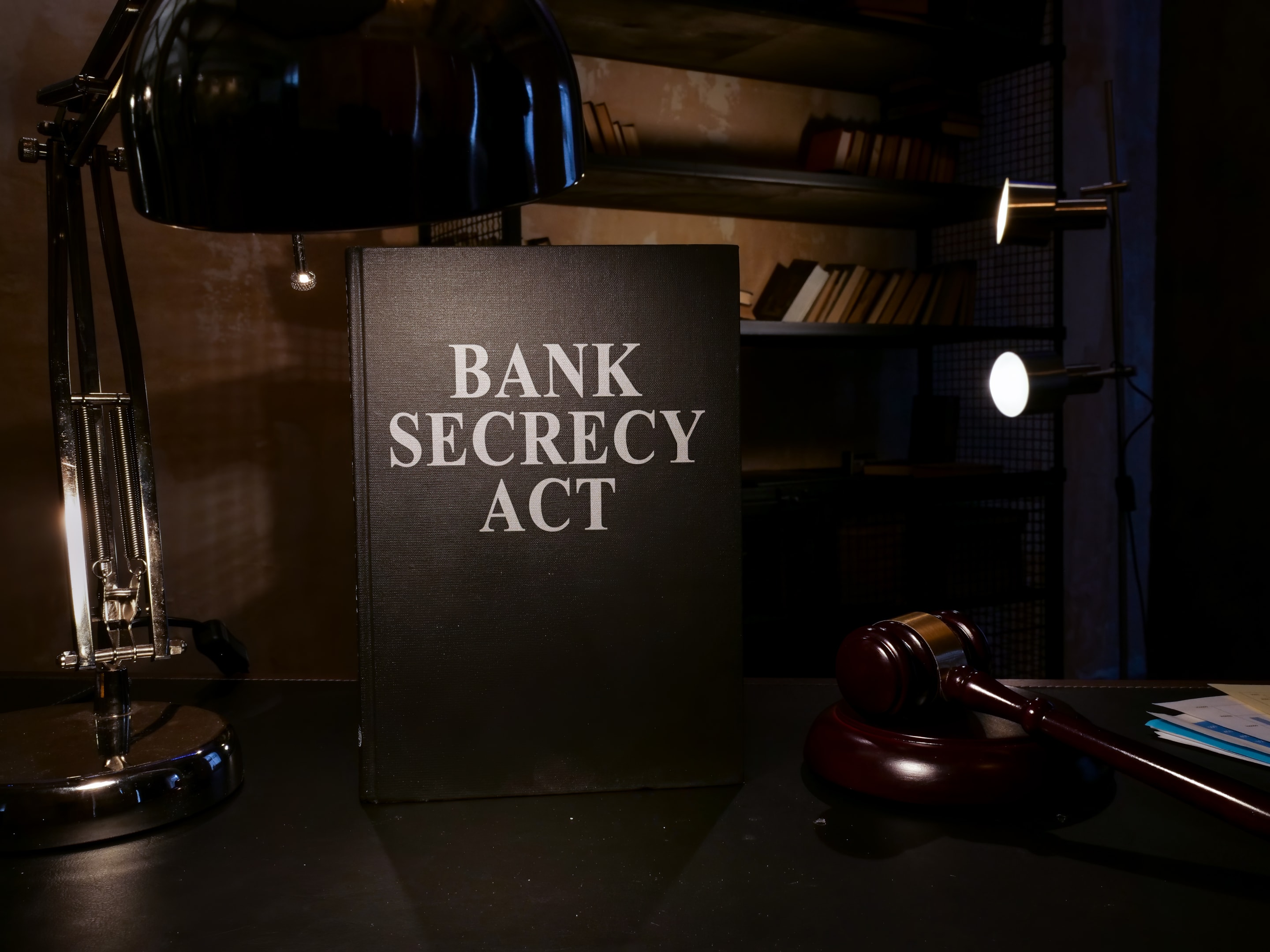

Understanding the Role of the Bank Secrecy Act (BSA) in Cannabis Banking

One of the main reasons banks won’t work with cannabis businesses is the Bank Secrecy Act (BSA). This act was passed in 1970 to combat money laundering by requiring financial institutions to keep records of cash transactions and file reports on activities that might be criminal.

When it comes to the cannabis industry, banks have to file a Suspicious Activity Report (SAR) for every cannabis account they manage, even if the business is compliant with local laws and state regulations. This is time-consuming, expensive, and comes with regulatory risk. For banks, this extra layer of compliance on top of the usual BSA requirements makes working with cannabis businesses not very attractive.

And then there’s the requirement to monitor cash purchases and daily aggregate amounts and the administrative burden on banks. Banks also have to make sure their clients aren’t doing tax evasion or money laundering. This super-compliance structure keeps many banks away from cannabis businesses.

FinCEN Guidance and the Fine Line Banks Walk in Cannabis Banking

The Financial Crimes Enforcement Network (FinCEN), a department of the Treasury, issued guidance to help banks work with cannabis businesses. This guidance outlines a few different types of SARs banks have to file depending on the client’s activity, including “marijuana limited” for compliant businesses and “marijuana priority” for accounts that raise red flags.

But FinCEN’s guidance wasn’t exactly a go-ahead. Banks still have to report suspicious activity even if the cannabis company is compliant.

The Drug Enforcement Administration (DEA) still considers cannabis a drug and banks feel they are walking a tightrope. Compliance costs are piling up and each filing and reporting requirement adds to the load and one misstep could be disastrous.

For most financial institutions the risk and resources required to maintain cannabis accounts under the current structure don’t justify the benefits. Unless cannabis is removed from the Controlled Substances Act at the federal level, many banks won’t enter the cannabis banking space.

Anti-Money Laundering (AML) and the Cannabis Industry

Anti-money laundering (AML) laws are a big obstacle for financial institutions looking to work with cannabis businesses. Under AML regulations, banks can’t touch money related to criminal activity which at the federal level includes cannabis sales. This prohibition puts financial institutions in a tough spot as they risk severe penalties if they accidentally or intentionally deal with cannabis funds.

Since cannabis is illegal federally, regulators could interpret any cash transaction from a cannabis business as money laundering. Banks therefore have to be extremely careful not to even appear to be enabling criminal activity which is why most have avoided serving the industry.

According to the Congressional Research Service (CRS) “a bank employee could face a 10-year prison term and criminal money penalties for knowingly receiving deposits or allowing withdrawals of $10,000 or more in cash derived from the distribution or sale of marijuana.” This personal liability and criminal risk only add to the banks’ hesitation to work with cannabis businesses.

In short, until cannabis is legalized or rescheduled at the federal level, AML laws will continue to keep financial institutions out of funds tied to cannabis sales leaving many cannabis businesses unable to get basic banking services.

The Cost of Reporting Suspicious Activity

One of the biggest obstacles for banks in serving cannabis-related businesses is the requirement to report suspicious activity constantly. Every single cash transaction related to cannabis has to be tracked. Even ordinary financial activity by a cannabis client can trigger a suspicious activity review which means filing costs, regulatory scrutiny, and resource drain on the institution.

This gets even more complicated when you add in cash purchases which are common in the cannabis industry since there is no traditional banking. For banks, the sheer volume of currency transactions means countless SARs which is impossible to manage without a huge financial burden. Banks can manage one or two accounts like this but not an entire portfolio.

To put it simply banks are forced to treat cannabis businesses with a level of suspicion they wouldn’t apply to other businesses. So why would a bank invest so much in the administrative burden and regulatory risk of cannabis banking?

They won’t.

Why Full Removal from the Controlled Substances Act May Be Necessary

As long as cannabis is a controlled substance even at Schedule III banks won’t open up fully to the industry. Moving to Schedule III may be a symbolic win and open up some new doors for cannabis businesses in terms of insurance and research but it won’t make a big difference in banking.

Why?

Banks need to be assured they won’t get penalized for working with cannabis. For that to happen the federal government would need to declassify cannabis from the Controlled Substances Act entirely. A full removal would mean cannabis-related businesses could be treated like any other legitimate industry and financial institutions could engage without fear of regulatory reprisal.

Schedule III still treats cannabis as a substance to be regulated and monitored. As long as that’s the case banking will still be a challenge for cannabis businesses.

Cannabis Businesses and the Need for Action

With limited banking cannabis businesses are forced into a cash-only world, high fees, and increased security risks. Handling large amounts of cash is dangerous and expensive and adds to the already complicated regulations. Plus no access to basic financial tools stifles growth, limits resources discourages investment, and hurts the entire industry.

Many in the cannabis industry are calling on Congress to pass legislation that would give banks a clear green light to work with cannabis businesses without fear of punishment. The SAFE Banking Act has been proposed to address this but has been delayed and stalled in the legislative process.

Conclusion: What This Means for Financial Institutions

Cannabis banking is a multi-layered issue of federal regulations, compliance requirements, and industry-specific challenges. Rescheduling cannabis to Schedule III may seem like progress but it’s not what the cannabis industry really needs to succeed.

Until cannabis is fully removed from the Controlled Substances Act financial institutions will remain gunshy. In the meantime, cannabis-related businesses will continue to face hurdles, using workarounds, cash-only operations, and high fees to navigate the current banking landscape.

So while a change in scheduling is good news it’s not the solution. The real solution is more comprehensive legislation that recognizes cannabis as a legitimate mainstream industry – one that deserves the same access to financial services as any other business. Until then the cannabis industry will be stuck in limbo waiting for the day they can bank like everyone else.

Get 20% off your first order and a free 2-pack of Delta 8 gummies!